Introduction

In the last year, we’ve written about the poor performance of clean energy, while highlighting the strong long-term outlook for the sector and the attractive valuations. 1 These are typically the sorts of things we focus on…valuations and the long-term fundamental prospects for companies. We tend to shy away from overanalyzing short-term market dynamics.

However, the pricing in clean energy has become increasingly perplexing and worthy of comment. In this piece, we’ll look at some of the recent head-scratching market moves, discuss the divergence between valuations and earnings expectations, and touch on conditions that can lead to dislocations like this.

Heads you win, tails I lose

Our founder Jeremy Grantham has often remarked that the market is good at determining the direction in response to new information, but it’s bad at determining the appropriate magnitude. In the clean energy sector, we’re starting to question the market’s ability to determine even the proper direction.

Much of the recent negative sentiment in clean energy has been driven by interest rates. High interest rates make renewable energy projects less attractive due to higher financing costs and lower discounted cash flows. With interest rates hovering around 23-year highs, the rate environment has been a drag on sentiment. When it comes to valuing companies, what should matter are interest rates over the next 30 or so years, but it’s hardly surprising that the market would extrapolate current conditions. Markets tend to do that when faced with uncertainty.

What’s more surprising is that clean energy has gotten hammered on news that implied a “higher for longer” rate environment and on September’s bigger than expected rate cut. In January, February, and March, CPI came in just slightly above expectations, and the WilderHill Clean Energy Index promptly tanked, on average losing to the MSCI All Country World Index (ACWI) by 3.7% on the days the data was announced. Yet, when the Fed cut rates by more than expected in September, the WilderHill Clean Energy Index promptly fell 3.1% between the 2 pm release and the end of the day. By the end of the following trading day, the WilderHill Clean Energy Index had underperformed ACWI by 3.6% since the announcement, eerily similar to its underperformance on the days earlier in the year when CPI came in above expectations.

The U.S. presidential election has also impacted sentiment, and once again, it seems that the market has been interpreting all news as bad news. When Joe Biden bombed in the June debate, increasing the probability that Donald Trump and his “Green New Scam” platform would gain favor with voters, the WilderHill Clean Energy Index trailed ACWI by 3.3% the following day. A couple weeks later the former president was shot in the ear and rallied his supporters by pumping his fists as he was ushered away to receive medical attention. The general perception was that this would cement his candidacy, and the market slapped the WilderHill Clean Energy Index down 5.7% in a flat market the next trading day. 2

Makes sense so far. Donald Trump has railed against the Inflation Reduction Act (IRA), and when his odds of winning the election go up, clean energy goes down. But it stands to reason that Kamala Harris’s entrance into the race and subsequent momentum should be perceived as good for clean energy. After all, the odds of a supportive administration have risen substantially. Yet, from when Biden dropped out of the race through the end of September, the WilderHill Clean Energy Index dropped 7.3% in an equity market (ACWI) that rose 5.5% – underperformance of almost 13%.

Clean energy seems to have landed in a spot where it loses no matter what.

Fundamentals matter…right?

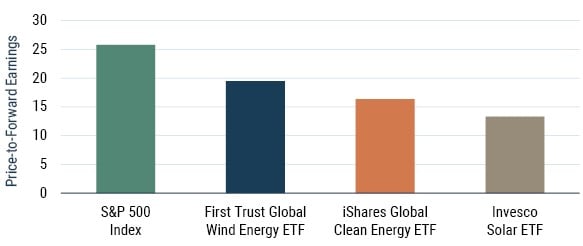

The poor performance has left valuations in deeply discounted territory (see Exhibit 1). The Invesco Solar ETF trades at around a 50% discount to the broad market, while the First Trust Global Wind Energy ETF and the broader S&P Global Clean Energy Index come in around 25% and 40% discounts, respectively. These valuations are particularly striking if you consider the growth prospects of these companies.

Exhibit 1: Despite Superior Growth, Clean Energy Companies Trade at a Large Discount

As of 9/30/2024 | Source: Bloomberg, GMO

The recent performance and depressed valuations imply weak expectations for fundamentals. However, many clean energy companies are expected to grow earnings considerably in the coming years. Analysts anticipate solar industry leaders like First Solar, Enphase, and Array Technologies to grow earnings per share (EPS) by 59%, 151%, and 47%, respectively, in 2025 vs. 2024. Expectations for biofuel flagbearers Darling Ingredients and Neste are equally impressive at 50% and 109%, respectively, while Vestas Wind Systems, the biggest wind turbine manufacturer in the world, is expected to register 151% EPS growth. Not to be outdone, LG Chem, one of the world’s largest lithium-ion battery manufacturers, clocks in with impressive 176% EPS growth expectations. 3

Admittedly, 2024 earnings look weak as they reflect what is seen as a cyclical bottom, but most of these companies are expected to earn significantly more next year than they did a couple years ago before the downturn in the cycle, and all of them are forecast to do substantially better in 2026. The important point here is that these are not flailing companies and industries. In fact, they are growing…and growing rapidly in many cases. Yet, the market is pricing these high growth companies as if they are destined to undergrow the market…or perhaps even shrink.

How can a dislocation like this occur?

We believe a couple factors have contributed to what appears to us to be a major mispricing. The first factor is that clean energy is a trivial portion of the major market indices. Clean energy companies are volatile and scary…and small. If they’re not in your benchmark, there’s little incentive to take the risk of investing in them. In fact, they’re only risky if you invest in them. If you have a substantive exposure to clean energy and it drops 30%, as it has this year, get ready for some tough questions. However, if the sector goes up 300% and you’re not invested, it’s highly unlikely that anyone will think to mention it.

The second, related factor is that there seem to be few long-only, long-term investors in clean energy these days. We recently asked a sell-side analyst a question about the long-term competitive advantages of a major solar company, and they began their response by noting that they receive “few to zero” questions about the company’s long-term prospects. Over and over, we hear that investors in clean energy are “playing the quarter” and that other investors are waiting on the sidelines for performance to turn or awaiting clarity on the U.S. presidential election before looking at the sector. 4 Given the short-term focus, it’s not surprising that the long-term prospects for the companies aren’t reflected in prices.

Conclusions

Clean energy stocks have recently been punished for both good and bad news. This has left valuations depressed and disconnected from the strong prospects many of these companies have. There are a variety of catalysts that could raise the sector out of its doldrums, 5 but that’s not the point of this piece. Even without catalysts, we believe many clean energy companies are positioned to generate strong returns going forward. While markets can be dislocated in the shorter-term, ultimately prices reflect an asset’s cash flow generation power.

The history of clean energy is littered with booms and busts, but we don’t think that its prospects are particularly risky at this point. Costs have come down, policy support continues to strengthen, and the industries are maturing. The market has been slow to recognize this evolution, which gives investors focused on the long-term an edge. We believe that a variety of clean energy companies have tremendous upside from here, and we strive to capitalize on these opportunities.

Appendix

Would a Trump Presidency Be Bad for Clean Energy?

The market seems convinced that a Trump presidency would be bad for clean energy, but it’s far from clear that that’s the case. While the former president has publicly threatened to “terminate” the IRA should he be elected, he’s also claimed to be a “big fan of solar,” that he’s “for electric cars,” and that he will prioritize the U.S. production of rare earth minerals – a critical input for many clean energy solutions.

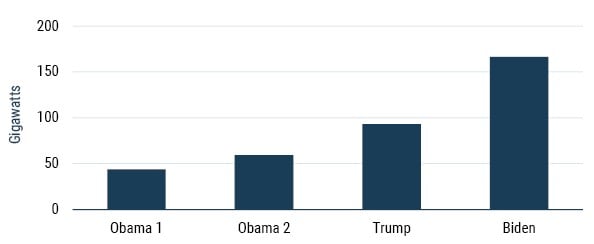

We won’t try to decipher his intentions, but we know from history that clean energy can thrive under Donald Trump’s leadership. During his term in office from January 2017 through December 2020, renewable activity sped up (see Exhibit 2) and the WilderHill Clean Energy Index rose 500%. In contrast, from the beginning of Joe Biden’s term in January 2021 through the end of September 2024, the WilderHill Clean Energy Index fell almost 80%. Not many investors would have expected those numbers ex-ante!

Exhibit 2: U.S. Clean Energy Capacity Additions by Presidential Term

Source: BloombergNEF | Obama 1: 2009 - 2012; Obama 2: 2013 - 2016; Trump: 2017 - 2020; Biden: 2021 - Present

Complicating matters even more for those who like simple answers, a large proportion of the economic growth and job creation driven by the IRA has been generated in predominantly Republican states. As you might imagine, this economic activity hasn’t gone unnoticed, and a group of 18 Republican congressmen reacted to Trump’s anti-IRA rhetoric by penning a letter to the Speaker of the House referring to repeal of the IRA as a “worst-case scenario.”

While we suspect the market would initially punish clean energy stocks if Trump wins the election, the driving forces behind adoption revolve around economics and the urgency to decarbonize, not politics. The market reaction to a potential Trump presidency seems to be more evidence that clean energy investors are focused on short-term sentiment rather than long-term fundamentals.

Download article here.

The views expressed are the views of Lucas White through the period ending October 2024 and are subject to change at any time based on market and other conditions. This is not an offer or solicitation for the purchase or sale of any security and should not be construed as such. References to specific securities and issuers are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations to purchase or sell such securities. Past performance is no guarantee of future results.

Copyright © 2024 by GMO LLC. All rights reserved.

See Turbulence on the Path to Transformation (September 2023) and Timing Your Swing (April 2024).

See Appendix for thoughts on whether the market has overreacted to the possibility of another Trump presidency.

The Focused Equity team held the stocks noted in this paragraph across a variety of investment strategies as of 9/30/2024. Earnings per share numbers are based on consensus Bloomberg estimates for adjusted earnings per share as of 9/30/2024.

Once again, see Appendix on whether the election deserves this much respect in pricing these companies.

Interest rates dropping, public policy (the U.S. IRA, the European Green Deal Industrial Plan, China, etc.), AI/data center energy demand, falling costs, inventory stabilization, and increased climate urgency are a few likely clean energy catalysts.